Long-run crop value versus fertiliser affordability.

Explore curated views from ADM’s Fertiliser Affordability Tracker, analysing feed wheat and oilseed rape values relative to delivered UK fertiliser prices. These charts are designed to help put current market levels into context and support more informed purchasing decisions.

Market Comment

Following continual escalation in the ME we have revised all of our domestic delivered value up. Nitrogen has led this trend with the N complex rising on the index an average of 20.9% since the February assesment.

Feed Wheat versus nitrogen affordability

Long-run indexed comparison showing how delivered UK nitrogen values have moved relative to feed wheat over time. Values are normalised to 100 from February 2018.

OSR versus DAP historic percentile

Shows where current phosphate affordability sits versus the long-run observed range. For example a value of 0.8 means the current ratio is higher than 80% of past observations in that same selected series.

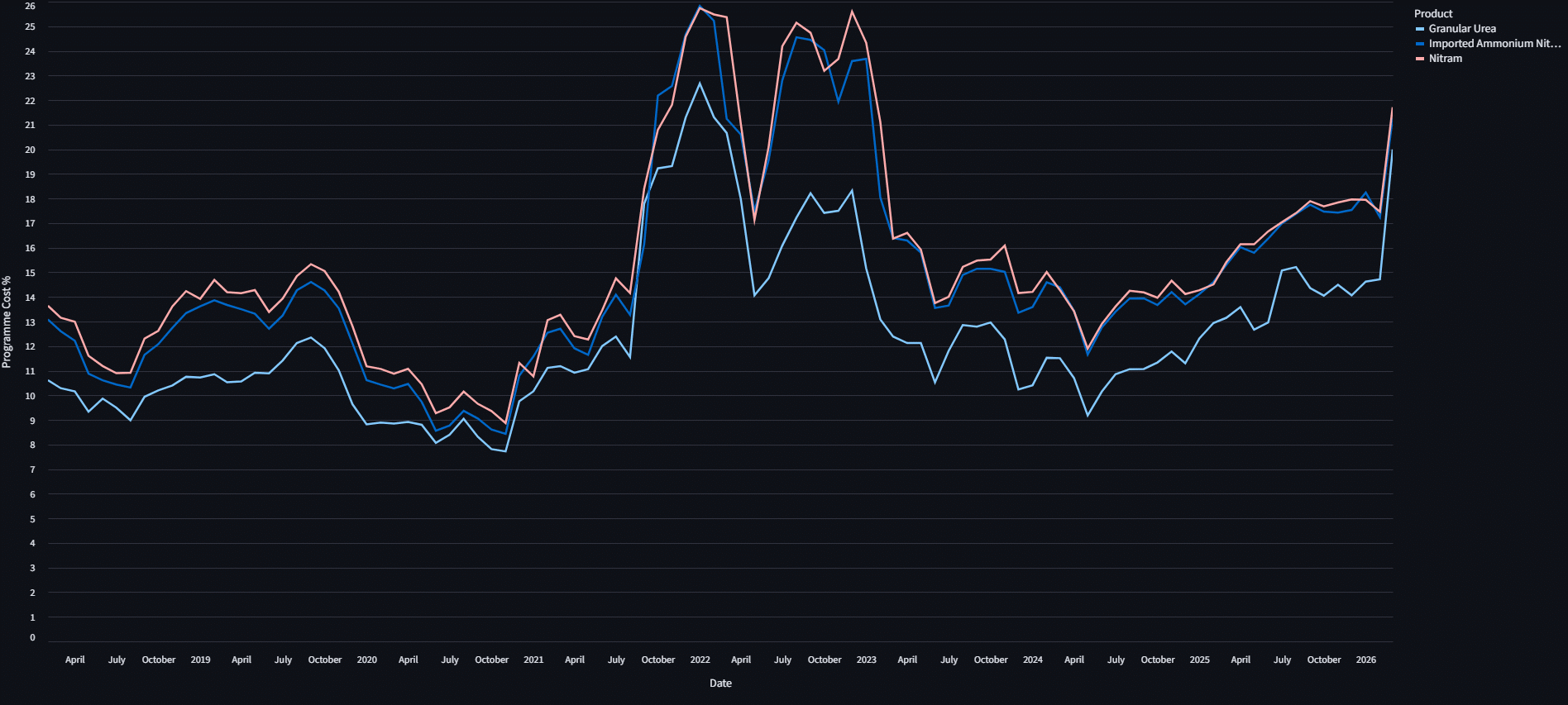

Programme cost burden versus crop value

Estimated Nitrogen cost as a percentage of crop revenue through time.

OSR relative affordability index versus Straights

Tracks the change in straights (DAP,TSP,MOP) affordability relative to oilseed rape from the base period.

Feed Wheat relative value z-score

Standardised view of whether current affordability sits rich or cheap versus history.

OSR Crop Price versus Nitrogen Price

Nitrogen price divided by the crop price on the same date. Values above 1 indicate the fertiliser is more expensive per tonne than the crop.

What this analysis shows

The tracker is designed to move beyond flat price and help place the market into commercial context.

Relative affordability

Compares fertiliser prices against crop values rather than looking only at outright market levels.

Historic context

Uses long-run indexed views, percentiles and z-scores to show whether markets are relative to historic values. Reference point for Feed Wheat is 8.5mt / ha Yield & 220kg of N applied / ha. Reference point for Oilseed Rape is 3.5mt /ha Yield & 180kg of N applied / ha.

Decision support

Helps growers and farm businesses assess timing, relative value and affordability as markets evolve.

Need a specific dataset or market view?

If there is a particular comparison, crop view, region or affordability measure you would like included in future updates, please contact Nico Papworth.